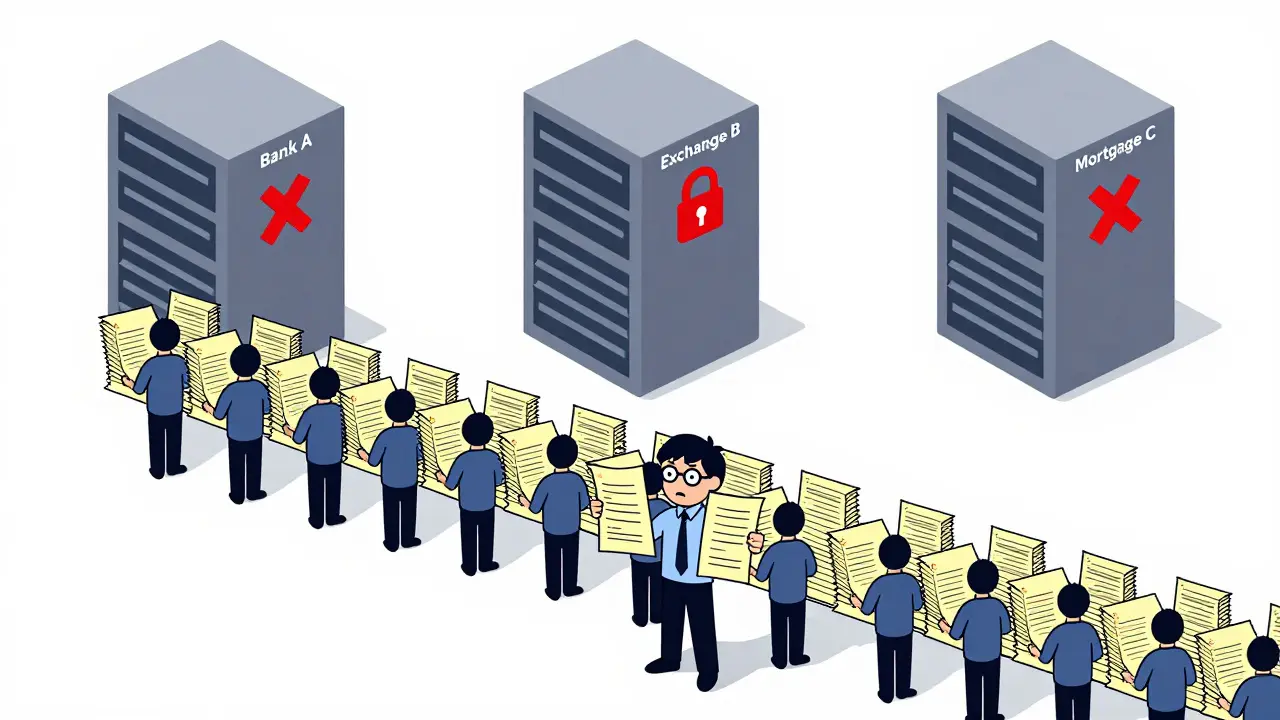

Imagine opening a bank account, signing up for a crypto exchange, and applying for a mortgage. Now imagine having to upload your passport, proof of address, and income statements three separate times. Each institution sits on its own server, re-verifying the same data you already proved months ago. This redundancy costs the global financial industry billions annually and frustrates customers who just want to get things done.

Enter decentralized KYC. It is not just a buzzword; it is a structural shift in how we handle identity verification. By moving from siloed databases to shared, secure blockchain networks, institutions can verify once and share trust many times. As of 2026, this technology is moving out of pilot programs and into live production environments, driven by skyrocketing compliance costs and stricter privacy laws.

The Problem With Traditional Identity Checks

Traditional Know Your Customer (KYC) processes are built on a legacy model that feels increasingly outdated. Banks and fintechs operate in isolation. When you open an account at Bank A, they collect your documents, run checks against sanctions lists, and store that data. If you then go to Bank B, the process starts from zero. There is no standard way for Bank B to say, 'Bank A already verified this person's identity last week.'

This fragmentation creates massive inefficiencies. In 2022 alone, global fines for Anti-Money Laundering (AML), KYC, and sanctions violations hit $8 billion USD. These penalties aren't just about bad actors slipping through; they often stem from administrative failures and inconsistent data management across fragmented systems. Furthermore, the operational cost is staggering. Redundant verification checks account for 30-40% of total KYC operational costs in traditional setups. For a customer, this means weeks of waiting. For a bank, it means bloated overheads and compliance fatigue.

| Feature | Traditional KYC | Decentralized KYC |

|---|---|---|

| Data Storage | Siloed, centralized databases per institution | Distributed ledger with off-chain sensitive data |

| Verification Frequency | Repeated for every new service provider | Once, with reusable proofs |

| User Control | Institution holds all data | User controls access via digital wallet |

| Onboarding Time | 2-3 weeks typical | 3-5 days in pilot implementations |

| Cost Efficiency | High due to redundant labor | Lower via shared infrastructure |

How Decentralized KYC Actually Works

At its core, decentralized KYC relies on three technical pillars: Verifiable Credentials (VCs), Decentralized Identifiers (DIDs), and smart contracts. Let’s break down what these mean in plain English.

Verifiable Credentials are digital equivalents of physical IDs. Think of them as encrypted diplomas or driver’s licenses issued by a trusted authority (like a government or bank). They contain claims about you-your name, age, or creditworthiness-that can be mathematically proven without revealing unnecessary details.

Decentralized Identifiers (DIDs) are unique strings that identify you on the blockchain. Unlike an email address or social media handle controlled by a corporation, a DID is yours. You manage the keys that control it. This ensures no single company can de-platform your identity.

When you need to prove your identity to a service provider, you don’t send them your raw passport scan. Instead, your digital wallet uses Zero-Knowledge Proofs (ZKPs) to generate a cryptographic proof. This proof confirms you meet the criteria (e.g., "I am over 18") without exposing your actual birthdate or ID number. The service provider verifies this proof against the issuer’s public key on the blockchain. The result? Instant verification with minimal data exposure.

Platforms like Catalyst Blockchain Manager and SelfKey have built enterprise-grade architectures around these concepts. Catalyst focuses on streamlining automation for banks, providing a 'single golden copy' of client data that syncs across consortium members. SelfKey takes a more user-centric approach, functioning as a self-sovereign identity network where users store their data locally on their devices and selectively disclose it.

Real-World Impact: Speed, Cost, and Security

Theoretical benefits are nice, but do they hold up in practice? Recent case studies suggest yes. JPMorgan Chase ran a pilot involving 15,000 corporate clients across 12 countries. The results were stark: a 47% reduction in KYC processing time and 33% cost savings compared to their traditional methods. Relationship managers praised the elimination of duplicate data entry, which had previously bogged down cross-border deals.

Similarly, the European KYC Utility, a consortium of 22 major European banks, reported 60% faster onboarding for cross-border corporate clients while maintaining 100% regulatory compliance. These numbers matter because speed directly correlates with revenue. Faster onboarding means fewer dropped leads and quicker capital deployment.

Security is another critical factor. Blockchain’s immutability means that once a verification record is added, it cannot be altered retroactively. However, true security also requires privacy. This is why sophisticated implementations use confidential computing environments. Institutions view the verification status (green light/red light) without accessing the raw underlying documents. As noted in AiPrise’s 2025 technical whitepaper, this achieves 'transparency with control,' balancing audit requirements with GDPR-style privacy mandates.

The Hurdles: Interoperability and Regulation

If decentralized KYC is so superior, why isn’t everyone using it yet? The answer lies in complexity. Implementing this technology is not a plug-and-play upgrade. It requires significant organizational preparation.

First, there is the issue of interoperability. Different blockchains speak different languages. Getting Bank A on Hyperledger Fabric to talk seamlessly with Exchange B on Ethereum requires robust API integration and standardized data schemas. Reddit discussions among fintech developers highlight that consensus-building alone can take 14 months, with teams struggling just to agree on basic data standards among three participating banks.

Second, regulatory uncertainty remains a barrier. While the EU leads in adoption (58% of major banks), other regions lag behind. Jurisdictions with strict data localization laws struggle with the distributed nature of blockchain. Professor Angela Walch of the University of Texas School of Law criticized current implementations in March 2025, noting they 'create new attack surfaces without adequately addressing the fundamental privacy paradox.' She argues that if the system fails, users lose access to their identities entirely-a risk central systems mitigate through customer support channels.

Performance is also a consideration. Deloitte’s 2025 report found that while sophisticated implementations achieve 99.98% data integrity, they suffer from 35-40% slower query response times during peak loads compared to centralized databases. For high-frequency trading platforms requiring millisecond decisions, this latency is unacceptable. For most banking operations, however, it is manageable.

Adoption Landscape in 2026

As of late 2025, the decentralized KYC sector captured approximately 8-12% of the $1.2 billion KYC technology market. The growth trajectory is steep, with a Compound Annual Growth Rate (CAGR) of 28.7%. Who is leading the charge?

- Enterprise Platforms: Catalyst and R3’s Corda KYC dominate with 65% market share. They offer the stability and regulatory alignment big banks demand.

- Crypto-Native Solutions: SelfKey and Civic cater to Web3 users and exchanges, prioritizing user sovereignty and ease of integration with digital wallets.

- Consortium Models: Groups like IDUnion and the European KYC Utility focus on collaborative governance, allowing competitors to share infrastructure without sharing proprietary business secrets.

Adoption rates vary significantly by institution size. Tier-1 banks lead with 43% implementation or piloting rates, according to the BIS Innovation Hub’s November 2025 survey. Regional banks trail at only 12%, largely due to higher relative implementation costs and smaller IT teams. Geographically, the European Union leads, followed closely by Singapore (49%) and the United States (37%). Regulatory sandboxes in these regions have been crucial in accelerating safe testing grounds.

What Comes Next? The Roadmap to 2030

The future of decentralized KYC looks increasingly integrated with broader financial infrastructure. Three developments will define the next two years.

- Standardization: The W3C Decentralized Identifier Working Group expects to finalize standard verifiable credential formats by Q3 2026. This will reduce the friction of cross-platform compatibility.

- CBDC Integration: Central Bank Digital Currencies (CBDCs) require real-time identity verification. Pilots by the Bank of England and Swiss National Bank in 2026 aim to embed decentralized KYC protocols directly into currency transactions.

- AI-Enhanced Risk Scoring: Combining blockchain-verified identity with behavioral analytics allows for dynamic risk assessment. The Monetary Authority of Singapore’s Project Ubin Phase 6 demonstrated this hybrid approach, offering continuous monitoring rather than one-off checks.

Gartner predicts that by 2027, three to four major enterprise platforms will control 75% of the market. Niche players will survive by focusing on specific verticals like trade finance or crypto exchanges. McKinsey rates the technology as 'high viability' for institutional banking but notes challenges remain for retail applications due to user experience hurdles. Ultimately, decentralized KYC won't replace traditional systems overnight, but it will become table stakes for any institution handling cross-border financial services by 2030.

Is decentralized KYC compliant with GDPR?

Yes, when implemented correctly. Because decentralized KYC keeps sensitive personal data off-chain and uses zero-knowledge proofs, it minimizes data retention risks. Users maintain control over their data, aligning with GDPR principles of data minimization and user consent. However, institutions must ensure their jurisdiction-specific data vaults comply with local storage laws.

How long does it take to implement a decentralized KYC solution?

Implementation typically involves three phases: consortium formation (3-6 months), technical integration (2-4 months), and user training (4-8 weeks). Total timeline ranges from 6 to 12 months depending on legacy system complexity and partner coordination. Compliance teams usually require 6-8 weeks to become proficient with new tools.

What are the main security risks of decentralized KYC?

Primary risks include private key loss by users (which can lock them out of their identity), smart contract vulnerabilities, and potential DDoS attacks on node networks. Additionally, if the initial issuing authority is compromised, fraudulent credentials could enter the system. Robust multi-signature governance and regular audits mitigate these risks.

Can small businesses afford decentralized KYC?

Currently, it is more accessible via SaaS models provided by large platforms like Catalyst. While upfront setup costs are high for building custom solutions, joining existing consortiums reduces individual burden. Small businesses benefit indirectly as larger partners adopt the tech, reducing friction in B2B transactions.

Which industries are adopting decentralized KYC first?

Corporate banking, cross-border payments, and cryptocurrency exchanges are early adopters. These sectors face the highest friction and regulatory scrutiny regarding identity verification. Insurance and healthcare are emerging markets, leveraging VCs for patient history and policyholder verification.

Finance

Finance

Joshua Alcover

May 25, 2026 AT 14:00The epistemological framework underlying decentralized identity verification necessitates a rigorous interrogation of the ontological status of digital sovereignty. We must consider if the mere cryptographic assertion of selfhood constitutes genuine identity or merely a simulacrum thereof. The paradigm shift from centralized hegemony to distributed consensus is not merely technical but profoundly philosophical, challenging the very notion of institutional authority in the post-truth era.

Diana Morris

May 26, 2026 AT 00:57stop overthinking it just use the tech and save time why are we still doing manual checks in 2026 its insane

Dianne Wright

May 26, 2026 AT 13:58i mean obviously everyone knows this already but like seriously banks are so slow they dont even realize how much money they are losing by making you send the same passport scan five times it is literally pathetic and i am tired of explaining basic logic to people who should know better

Christina Pearce

May 27, 2026 AT 04:14This is such an interesting perspective on how blockchain can streamline our daily financial interactions. I really appreciate how the article breaks down the technical aspects without being too overwhelming. It makes me wonder how soon we might see this implemented in smaller regional banks rather than just the big tier-1 institutions mentioned here.

Barclay Chantel

May 27, 2026 AT 23:01How quaint. Another techno-utopian fantasy sold to the masses by engineers who have never had to deal with the messy reality of human bureaucracy. The idea that 'trust' can be codified into a smart contract is laughable at best and dangerous at worst. You cannot algorithmize morality or accountability. This is just another way for Silicon Valley elites to erode privacy under the guise of efficiency while creating new points of failure that will inevitably be exploited by bad actors.

lorna erni

May 29, 2026 AT 16:47I think we can all agree that this technology has huge potential but we need to make sure it works for everyone not just the tech savvy folks in SF lets bring this to communities that actually need faster banking access because waiting weeks for a mortgage approval is unacceptable for anyone

stalin brian

May 30, 2026 AT 04:07hey guys i was reading about this in my country and we have similar issues with cross border payments taking forever would love to hear more about how other countries are handling the regulatory side of things since every place seems to have different rules

kamal ifrani

May 30, 2026 AT 12:56let me tell you something you absolute morons this system is going to collapse under its own weight because nobody understands the fundamental flaws in zero knowledge proofs when applied at scale its a disaster waiting to happen and i bet my last rupee that the first major hack will expose how vulnerable these wallets really are

Craig Swanson

May 31, 2026 AT 06:17Look, I get the skepticism but we have to acknowledge that the current system is broken beyond repair. If we don't move toward decentralized solutions, we're stuck in a loop of inefficiency and high costs. Let's focus on constructive dialogue about implementation challenges rather than tearing down the concept entirely. We can build a better future together if we approach this with an open mind.

mark valmart

June 1, 2026 AT 17:09i feel ya man its crazy how much hassle it is to just open a bank account sometimes i spend hours gathering docs only to get rejected for some minor detail

Crystal Davis

June 2, 2026 AT 14:07The statistical analysis presented here is fundamentally flawed due to selection bias in the pilot programs cited. JPMorgan's results are anecdotal at best and cannot be extrapolated to the broader market without controlling for variables such as existing IT infrastructure maturity. Furthermore, the claim of 33% cost savings ignores the substantial upfront capital expenditure required for blockchain integration which often exceeds traditional KYC upgrade costs by a factor of three.

Miss Masquer

June 3, 2026 AT 03:17I find it fascinating how the cultural context of privacy varies so significantly between regions, particularly when comparing the European emphasis on data protection with the more utilitarian approaches seen elsewhere, which leads me to believe that any global standard for decentralized identity must be incredibly flexible to accommodate these diverse societal values while still maintaining robust security protocols that protect individual users from exploitation.

trisya hazriyana

June 5, 2026 AT 03:14oh sure let's just hand over our identities to a blockchain because that never goes wrong lol the irony of using 'decentralized' tech to create a single point of failure in your private keys is lost on everyone except the paranoid ones who actually read the whitepapers

Debbie Lewis

June 6, 2026 AT 19:08just watching this unfold from the sidelines seems like a lot of hype but maybe it will work out eventually

Eric Grosso

June 7, 2026 AT 21:06does this mean i wont have to fax my drivers license anymore cause thats pretty wild to think about honestly

Edith Mair

June 8, 2026 AT 22:30We need to address the regulatory gaps immediately. The current lack of standardized legal frameworks for Verifiable Credentials creates significant liability risks for institutions adopting these systems. Without clear jurisdictional guidelines, companies are hesitant to invest heavily in infrastructure that may become obsolete or non-compliant within months.

Sam Dashti

June 9, 2026 AT 19:10Imagine a world where your identity is like a superpower key that unlocks doors without you having to show your ID card every single time it feels like magic but grounded in math which is pretty cool if you think about it

Joe Clements

June 10, 2026 AT 12:11I really hope this helps reduce the stress people feel during financial transactions. Knowing that your data is secure and that you have control over who sees it sounds like a relief for many of us who worry about identity theft and data breaches.

Rosie Morris

June 12, 2026 AT 11:43i totally agree with the sentiment here its just so frustrating to repeat the same process over and over again hopefully this tech will fix that mess