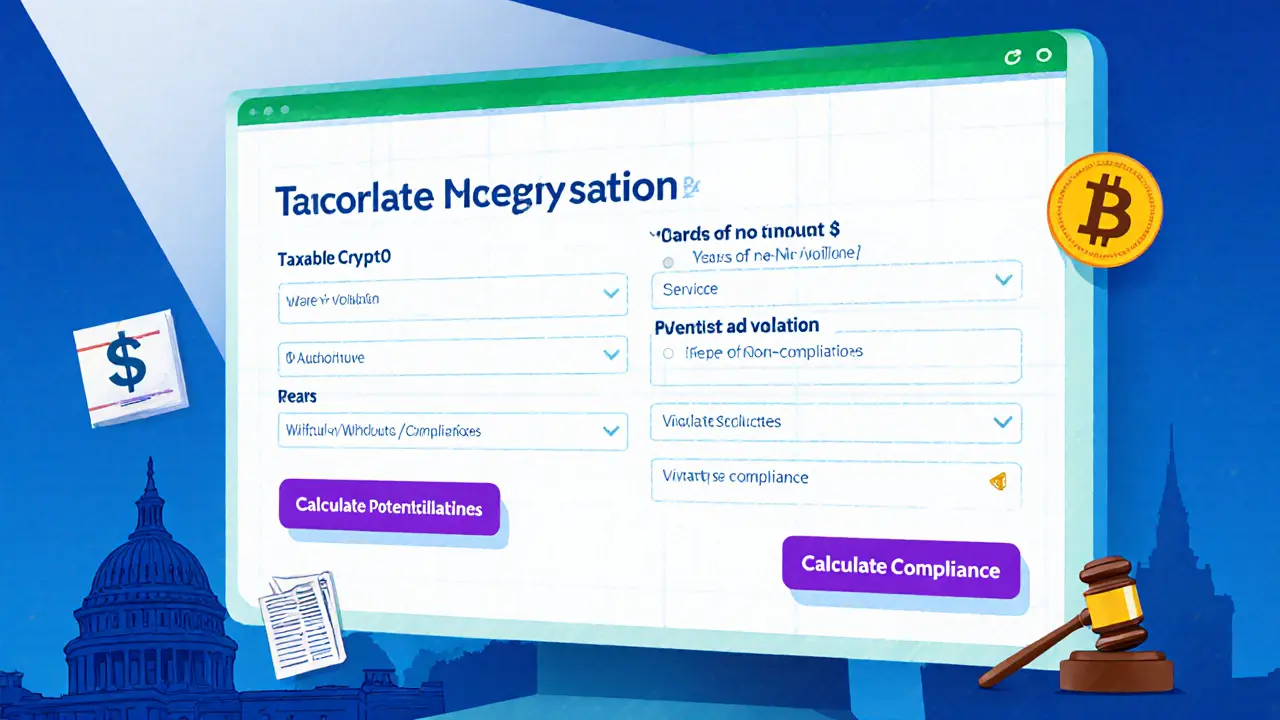

Crypto Tax Evasion Penalty Calculator

Enter values and click Calculate to see potential penalties

Criminal Penalties

Up to 5 years in prison and $250,000 fine per count

Civil Penalties

Up to 75% of unpaid tax plus interest

Quick Take

- U.S. law treats crypto like property, so every sale, trade, or receipt is taxable.

- Willful failure to report crypto income can lead to up to 5 years in prison and a $250,000 criminal fine.

- Civil penalties can add another 75% of the unpaid tax, plus interest.

- Since Jan12025, exchanges must file Form 1099‑DA, giving the IRS a near‑real‑time view of your transactions.

- Good record‑keeping and tax‑software (e.g., CryptoWorth, Koinly) are the cheapest way to stay safe.

What is crypto tax evasion?

When the Internal Revenue Service (IRS) says crypto is property, it means every move you make - selling Bitcoin, swapping Ether for a meme‑coin, mining new tokens, or even getting paid in crypto - creates a taxable event. If you deliberately hide those events or file a false return, you cross from a simple mistake into criminal tax evasion. The difference matters: civil non‑compliance is a paperwork problem; criminal evasion is a felony that can land you behind bars.

How the IRS is hunting down hidden crypto

The agency’s enforcement arm, Operation Hidden Treasure, uses blockchain analytics to follow the money trail through every major network. By scanning wallet addresses, transaction hashes, and exchange deposits, the IRS can match on‑chain activity to the information on tax returns.

Starting Jan12025, every U.S. crypto exchange is required to submit Form 1099‑DA. This form details every trade, purchase, and sale a user makes on the platform. The data feed turns what used to be an opaque market into a transparent ledger the IRS can query instantly.

Because the blockchain leaves a permanent, tamper‑evident record, the IRS can go back years to reconstruct omitted transactions - something impossible with cash‑based schemes.

Penalties you could face

The law sets a hard ceiling: up to five years in federal prison and a $250,000 fine for each count of criminal tax evasion. That figure applies whether you’re a lone trader or the CEO of a crypto‑focused startup.

Civil penalties stack on top of the criminal ones. The IRS can charge up to 25% for failing to pay tax, another 25% for failing to file, and interest that compounds daily. In the worst‑case scenario, you could owe 75% of the unpaid tax in penalties alone.

| Penalty Type | Maximum Prison | Maximum Fine | Additional Financial Impact |

|---|---|---|---|

| Criminal (felony) | 5 years | $250,000 | Potential asset seizure, restitution |

| Civil - Failure to Pay | None | Up to 25% of unpaid tax | Interest accrues daily |

| Civil - Failure to File | None | Up to 25% of unpaid tax | Interest accrues daily |

Typical mistakes that turn into evasion

Most people who end up in trouble didn’t set out to break the law. They simply missed a reporting requirement.

- Ignoring small transactions. The IRS says even a $10 trade must be reported.

- Failing to track self‑transfers. Moving coins between your own wallets changes cost basis but isn’t a taxable event; it still needs documentation.

- Using the old “universal accounting” method after Jan12025. The new wallet‑by‑wallet accounting rule forces you to calculate basis per wallet, per token.

- Relying on exchange statements alone. Many platforms still don’t provide full 1099‑DA data for DeFi activities, staking rewards, or airdrops.

Tools that make compliance painless

Today’s market offers several dedicated crypto‑tax platforms. They pull transaction data via API, calculate gains using FIFO, LIFO, or specific identification, and generate the IRS‑ready Form 8949.

- CryptoWorth - strong for UK‑based users, provides dual‑currency reports.

- Koinly - offers real‑time syncing with over 300 wallets and exchanges.

- CoinLedger - focuses on audit trails and automatically flags missing documents.

Using one of these services can cut the time you spend on spreadsheets from days to minutes, and they produce the exact line items the IRS expects.

Real‑world stories: what went wrong and how they fixed it

Reddit’s r/Tax community is full of people who received the dreaded “CP2000” notice - a letter saying the IRS found income you didn’t report. One user, who had mined a modest amount of Bitcoin in 2022 and never reported the $3,200 fair market value, ended up with a civil penalty of 25% plus interest. After filing an amended return and paying the tax plus $600 in penalties, the IRS reduced the civil fine by 50% for voluntary compliance.

Another case involved a small trading firm that tried to hide $1.2million in crypto gains by filing a false Schedule D. The FBI, using blockchain analytics from Operation Hidden Treasure, traced the funds back to the firm’s wallets. The owners faced three counts of criminal tax evasion, got 18 months in prison, and were hit with the full $250,000 fine per count.

Both stories underline a simple rule: the sooner you come clean, the lower the financial hit and the less likely you’ll see a jail sentence.

Step‑by‑step plan to get back on track

- Gather every blockchain address you own - exchanges, hardware wallets, DeFi contracts.

- Export full transaction histories in CSV or JSON format. Most exchanges now include the required 1099‑DA fields.

- Choose a tax‑software platform (Koinly, CryptoWorth, etc.) and import the data.

- Run the cost‑basis calculator using the wallet‑by‑wallet method. Double‑check any self‑transfers for correct basis adjustments.

- Generate the IRS Form 8949 and attach it to an amended 1040 if you’re fixing past years.

- Pay the tax owed plus any calculated civil penalties. Consider a reasonable‑cause request to lower penalties if you’re acting in good faith.

- Keep the new records for at least seven years - the IRS can audit that far back.

If the numbers feel overwhelming, hire a CPA who specializes in digital assets. Their fee is usually a fraction of what a $250,000 fine would cost.

Frequently Asked Questions

Do I have to report a $5 cryptocurrency purchase?

Yes. The IRS treats every acquisition, even a $5 token, as a taxable event if you later sell or exchange it. The purchase itself isn’t taxable, but you must keep the cost basis for future calculations.

What is the difference between civil and criminal penalties?

Civil penalties are monetary charges for failing to pay or file taxes; they can reach up to 75% of the unpaid tax. Criminal penalties involve a felony conviction, possible imprisonment (up to 5 years), and a $250,000 fine per count.

Can I use crypto‑tax software for DeFi yields?

Most leading platforms now pull staking rewards, liquidity‑pool earnings, and airdrops directly from supported wallets. Make sure the tool you choose supports the specific protocol you used.

If I missed a year, should I file an amended return?

Absolutely. Voluntary compliance often reduces both civil and criminal penalties. The IRS looks favorably on taxpayers who come forward before an audit.

Will the new Form 1099‑DA make it impossible to hide crypto income?

It greatly narrows the anonymity window. Exchanges must now report every taxable transaction, so the IRS can match on‑chain data with filing records. While clever workarounds still exist, the risk of detection is far higher than before 2025.

Finance

Finance

Anthony R

September 18, 2025 AT 20:22Thanks for the thorough breakdown, it really clarifies the stakes, especially for those of us who are new to crypto taxation, and the emphasis on keeping detailed records is spot‑on, the penalty calculator is a handy tool, and the reminder about voluntary disclosure could save a lot of trouble.

Linda Welch

September 19, 2025 AT 13:02Oh great another horror story about the IRS, because nothing says "American freedom" like locking people up for trading Bitcoin, the whole thing is just a massive over‑reach and the fines are absurd yet somehow still look like a bargain compared to the alternative of a courtroom drama that lasts forever.

victor white

September 19, 2025 AT 21:22One can’t help but wonder whether the shadowy cabal behind the scenes is secretly orchestrating these enforcement drives, all while the everyday trader is left to navigate a labyrinth of regulations that seem designed to trap the unwary.

Rebecca Stowe

September 20, 2025 AT 11:16Hey folks, don’t let the scary headlines get you down! Staying on top of your crypto taxes is totally doable, especially with the right tools, and the peace of mind you’ll get is worth every minute you spend organizing your records.

Aditya Raj Gontia

September 20, 2025 AT 16:49Just use Koinly, it does the job.

Kailey Shelton

September 21, 2025 AT 03:56Don’t ignore the small trades; the IRS sees everything.

Angela Yeager

September 21, 2025 AT 10:52Exactly, even a $10 token sale counts. I recommend pulling all your exchange CSVs into a tax‑software like CryptoWorth; it auto‑calculates cost basis and generates the 8949, making filing a breeze.

vipin kumar

September 22, 2025 AT 02:09The IRS is just another crypto‑hater agency trying to crush innovation, but we can’t let them win by staying silent.

Vaishnavi Singh

September 22, 2025 AT 09:06Beyond the legal penalties lies a deeper ethical question: if we profit from a decentralized system, do we owe a duty to the collective? Ignoring tax obligations betrays that very principle.

mark gray

September 22, 2025 AT 22:59All that matters is keeping your paperwork straight; the IRS will catch up eventually, so better to be proactive than reactive.

Alie Thompson

September 23, 2025 AT 07:19When the government threatens to lock us up for simply holding digital assets, it sends a chilling message about liberty.

Citizens must understand that tax compliance is not merely a bureaucratic hurdle, but a moral contract.

The criminal penalties outlined-up to five years imprisonment and a quarter‑million dollars fine-are designed to deter willful deception.

Yet, many honest traders stumble into trouble because of ignorance, not malice.

Education, therefore, becomes the most effective shield against such draconian measures.

Utilizing reputable tax software can transform a confusing ledger into a clear, auditable record.

Platforms like Koinly or CryptoWorth automate cost‑basis calculations, sparing users endless spreadsheet battles.

Moreover, keeping meticulous records of every wallet transfer, even self‑moves, eliminates the gray areas that auditors love to exploit.

If a mistake does occur, the IRS often shows leniency to those who voluntarily disclose their errors.

A timely amended return, accompanied by reasonable‑cause documentation, can halve or even erase the civil penalties.

Conversely, attempting to hide assets only fuels the agency’s forensic efforts, which have become remarkably sophisticated.

Blockchain analytics, once the domain of hobbyists, are now wielded by seasoned investigators.

They can trace a fraction of a cent across multiple exchanges, linking it back to an individual taxpayer.

Thus, the notion that crypto offers absolute anonymity is a myth that the IRS repeatedly busts.

In the end, respecting the law while embracing innovation is the only sustainable path forward.

Donald Barrett

September 23, 2025 AT 23:59This whole crypto tax thing is a dumpster fire, and the IRS is just adding fuel.

Christina Norberto

September 24, 2025 AT 08:19Esteemed colleagues, allow me to articulate the gravity of the situation: the United States Treasury, in conjunction with its enforcement arm, has promulgated a regulatory matrix wherein non‑compliance invokes not merely pecuniary sanctions but also punitive incarceration, thereby underscoring the imperative for immediate and comprehensive remediation.

Fiona Chow

September 24, 2025 AT 22:12Sure, let’s all panic while the IRS silently watches our wallets and decides to raid our bank accounts.

Lara Cocchetti

September 25, 2025 AT 05:09The narrative they feed is a smokescreen; the real agenda is to control the decentralized economy and co‑opt the technology for surveillance.

Mark Briggs

September 25, 2025 AT 19:02Nice article, but I bet the real issue is that nobody reads the fine print.

mannu kumar rajpoot

September 26, 2025 AT 03:22Honestly, if you don’t keep meticulous records, you’re just asking for trouble; the system is rigged against the uninformed.

Tilly Fluf

September 26, 2025 AT 18:39While the penalties may appear daunting, I remain confident that with diligent record‑keeping and the appropriate use of tax‑software, compliance is entirely achievable.

Darren R.

September 27, 2025 AT 01:36Oh, the drama! Imagine the heartbreak when a seasoned trader faces a $250K fine-truly a tragedy of epic proportions.

Hardik Kanzariya

September 27, 2025 AT 15:29Friends, if you’re feeling overwhelmed, take a deep breath and start gathering your wallet addresses; you’ll find the process less scary step by step.

Shanthan Jogavajjala

September 27, 2025 AT 23:49From a technical standpoint, exporting CSVs and feeding them into an API‑compatible platform is a standard workflow that reduces manual errors dramatically.

Millsaps Delaine

September 28, 2025 AT 16:29One must recognize that the confluence of cutting‑edge digital assets and antiquated tax codes creates a fertile ground for both innovation and misinterpretation, a reality that demands both intellectual rigor and proactive stewardship.

Jack Fans

September 29, 2025 AT 00:49Hey there! If you’re looking for a quick start, try importing your transaction history into Koinly – it will auto‑generate the 8949 for you, which is a massive time‑saver!!

Adetoyese Oluyomi-Deji Olugunna

September 29, 2025 AT 14:42In the grand scheme of fiscal obligations, one might observe that the veritable labyrinth of crypto taxation, whilst ornate, remains not insurmountable; however, a diligent mind must circumvent the myriad pitfalls lest they fall prey to punitive ramifications.

Krithika Natarajan

September 29, 2025 AT 23:02I hear you; staying organized really does make a difference.